- Видео 559

- Просмотров 19 137 691

Bionic Turtle

США

Добавлен 18 дек 2007

Bionic Turtle is your expert resource and global community, specializing in professional certification: FRM, CFA, CFP, ERP, CAIA, Risk School. Visit our website at www.bionicturtle.com for more in-depth FRM materials! Make sure to take a quick second to subscribe to our page so you are notified when we post new videos!

The SML is a general CML (informal FRM tip series)

A forum member asked me this great question; "If the CML plots well-diversified portfolios, and well-diversified portfolios have no idiosyncratic risk, then isn't the CML also a plot of systematic risk (aka, beta)? Put another way, doesn't the CML already map to the SML?" My response is here forum.bionicturtle.com/threads/week-in-financial-education-2021-05-24.23840/post-88829

This mathematically explains why my favorite summary distinction of the difference between the CML and SML is this: the CML plots only (the most) efficient portfolios, but the SML plots all portfolios (including inefficient portfolios). I hope that's interesting!

Subscribe here ruclips.net/user/bionicturtle?sub-confir...

This mathematically explains why my favorite summary distinction of the difference between the CML and SML is this: the CML plots only (the most) efficient portfolios, but the SML plots all portfolios (including inefficient portfolios). I hope that's interesting!

Subscribe here ruclips.net/user/bionicturtle?sub-confir...

Просмотров: 5 966

Видео

Why par yields are the best interest rate measure

Просмотров 6 тыс.2 года назад

Par yields are the best interest rate because they summarize the spot rate term structure into a single yield measure. I also show the so-called "coupon effect" which is also an argument in favor of par yields. But I think the better reason is their information content. Yield to maturity (TYM) is also a single (constant) rate but YTM is a function of an observed bond price: the coupon effect ex...

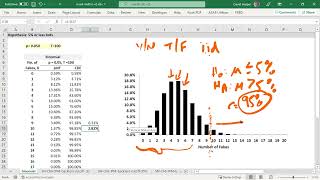

Binomial test: if Elon Musk samples 100 twitter accounts, how many bots (fakes) are too many?

Просмотров 4,6 тыс.2 года назад

Elon Musk is holding up his twitter purchase to investigate their claim that only 5.0% of the accounts on the platform are fake. If he samples 100 accounts, how many is too many; i.e., at what number should he reject the null hypothesis? Subscribe here ruclips.net/user/bionicturtle?sub-confirmation=1 to be notified of future tutorials on expert finance and data science, including the Financial ...

A conversation with Mark Meldrum, aka the GOAT (who has joined us at CeriFi by the way)

Просмотров 2,3 тыс.2 года назад

You probably already know Mark Meldrum because he is the arguably the best finance instructor on the planet. He's joined us at CeriFi, so stuff just go real. In this video, he talks. Then we talk. Subscribe here ruclips.net/user/bionicturtle?sub-confirmation=1 to be notified of future tutorials on expert finance and data science, including the Financial Risk Manager (FRM), the Chartered Financi...

CFA - Tackling Classic Duration Questions

Просмотров 3 тыс.3 года назад

For those of you studying for the L1 CFA exam, it’s crucial to be good at the fundamental topics. With that in mind, in this archived webinar Richie Owens, CFA, walks through how to tackle some of the classic duration questions you might face on the day. Subscribe here ruclips.net/user/bionicturtle?sub-confirmation=1 If you have questions or want to discuss this video further, please visit our ...

How To Study for the CFA Level 1 Exam

Просмотров 2 тыс.3 года назад

Why is The Dalton Accelerator™ for the CFA® Program right for you? Our resources include a robust video library with additional instructor perspectives and content. Intro videos that help you create your success strategy, overview videos for each of the topic areas, and skills videos aligned to various questions. These videos individually, or all together, will enhance your learning experience....

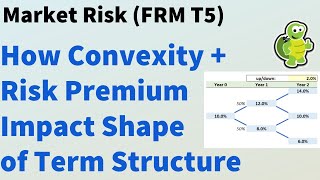

Convexity and risk premium impacts on shape of term structure (FRM T5-08)

Просмотров 7 тыс.4 года назад

In this video, I'm going to try to illustrate all of the important ideas that are in Tuckman's Chapter 8: The Evolution of Short Rates and the Shape of the Term Structure. This chapter discusses the shape of the term structure and the key influences on the shape of the spot rate term structure. I'll start with pure expectations, where the term structure will reflect only expectations about the ...

Risk-neutral probabilities (FRM T5-07)

Просмотров 19 тыс.4 года назад

One of the harder ideas in fixed income is risk-neutral probabilities. In this video, I'd like to specifically illustrate, and define, what we mean by risk-neutral probabilities. I will do this in three steps. The first one is just a simple example of a coin toss, where my objective is to illustrate what we mean by risk-neutral probabilities. These are the probabilities that equate the expected...

Rank Correlations: Spearman's and Kendall's Tau (FRM T5-06)

Просмотров 16 тыс.4 года назад

In this video, we will briefly review the Pearson correlation coefficient. Of course, that's the most popular measure of correlation, but mostly just so we have a baseline to compare to the two measures of rank correlations. Specifically, we will look at the Spearman's rank correlation and Kendall's tau rank correlation. These two are measures of ordinal correlation as opposed to a measure of c...

Value (VaR) Mapping a fixed-income portfolio (FRM T5-05)

Просмотров 11 тыс.4 года назад

In this video, we walk through an actual case study of Value at Risk (VaR) mapping, specifically as it is illustrated by Phillip Jorion in Chapter 11 of his book, Value at Risk. We will take a two-bond fixed income portfolio. It's going to have a value of 200 million, and we're going to look at VaR mapping under three different approaches. That mapping means that we'll take the value of the por...

Value at Risk (VaR) Backtest (FRM T5-04)

Просмотров 18 тыс.4 года назад

When we specify something like a 95% value at risk or 95% VaR, we mean that 95% is the confidence level and, therefore, 5% is the significance level. That means we expect on 5% of days for the actual loss to be worse than the VaR or to exceed the VaR. This video is about the backtest of a VaR, which is a very handy statistical tool that we have at our disposal to backtest or to test the validit...

Expected shortfall: approximating continuous, with code (ES continous, FRM T5-03)

Просмотров 6 тыс.4 года назад

In my previous video, I showed you how we retrieve expected shortfall under the simplest possible discrete case. That was a simple historical simulation, but that was discrete. In this video, I'm going to review expected shortfall when the distribution is continuous. Specifically, I will use the normal distribution, but you'll see when we look at the code that we can substitute other parametric...

Expected shortfall (ES, FRM T5-02)

Просмотров 24 тыс.4 года назад

In this video, I'm going to show you exactly how we calculate expected shortfall under basic historical simulation. Expected shortfall is both desirable and timely. It's desirable because it is coherent, satisfies all four conditions of coherence, including subadditivity, whereas var does not. Second, it's timely because you may know that in Basel IV, specifically fundamental review the trading...

Lognormal value at risk (VaR, FRM T5-01)

Просмотров 10 тыс.4 года назад

Welcome to the first video in this new playlist that is devoted to Topic 5 in the FRM. Topic 5, Market Risk, is the first topic in Part 2. We will start here by comparing normal to lognormal VaR and, specifically, we are going to generalize to absolute VaR. Absolute VaR generalizes the relative VaR so it's the complete version of VaR. The key thing that we are going to do here is look at four d...

R Programming Finance: Load historical stock price series (rfinance-01)

Просмотров 23 тыс.4 года назад

In this video, I'm excited to share one approach to importing historical stock price series into R. I think there are different ways to do this. My approach here is inspired by the approach that is illustrated by Jonathan Regenstein and his excellent book, Reproducible Finance with R, which you can find here: amzn.to/2zN6z1e. I will show you my variation and then the source from which I learned...

Level 1 Chartered Financial Analyst (CFA ®): Sampling and Estimation

Просмотров 4,1 тыс.4 года назад

Level 1 Chartered Financial Analyst (CFA ®): Sampling and Estimation

R Programming: Introduction: ggplot for capital market line (CML, R Intro-08)

Просмотров 2,4 тыс.4 года назад

R Programming: Introduction: ggplot for capital market line (CML, R Intro-08)

Level 1 Chartered Financial Analyst (CFA ®): Common Probability Distributions

Просмотров 6 тыс.4 года назад

Level 1 Chartered Financial Analyst (CFA ®): Common Probability Distributions

Fixed Income: Key rate shift technique (FRM T4-43)

Просмотров 8 тыс.4 года назад

Fixed Income: Key rate shift technique (FRM T4-43)

Level 1 Chartered Financial Analyst (CFA ®): Money Market Yields

Просмотров 4,5 тыс.4 года назад

Level 1 Chartered Financial Analyst (CFA ®): Money Market Yields

Fixed Income: Duration and Convexity Summary (FRM T4-42)

Просмотров 18 тыс.4 года назад

Fixed Income: Duration and Convexity Summary (FRM T4-42)

Level 1 Chartered Financial Analyst (CFA ®): Correlation, covariance and probability topics

Просмотров 3,6 тыс.4 года назад

Level 1 Chartered Financial Analyst (CFA ®): Correlation, covariance and probability topics

Fixed Income: Analytical Convexity; aka, modified convexity (FRM T4-41)

Просмотров 1,7 тыс.4 года назад

Fixed Income: Analytical Convexity; aka, modified convexity (FRM T4-41)

Level 1 Chartered Financial Analyst (CFA ®): Conditional, unconditional and joint probabilities

Просмотров 3,4 тыс.4 года назад

Level 1 Chartered Financial Analyst (CFA ®): Conditional, unconditional and joint probabilities

Fixed Income: Bullet versus Barbell Bond Portfolio (FRM T4-40)

Просмотров 8 тыс.4 года назад

Fixed Income: Bullet versus Barbell Bond Portfolio (FRM T4-40)

Level 1 Chartered Financial Analyst (CFA ®): Measures of dispersion including volatility

Просмотров 1,7 тыс.4 года назад

Level 1 Chartered Financial Analyst (CFA ®): Measures of dispersion including volatility

Fixed Income: Impact of Yield and Coupon on Duration and DV01 (FRM T4-39)

Просмотров 3,1 тыс.5 лет назад

Fixed Income: Impact of Yield and Coupon on Duration and DV01 (FRM T4-39)

R Programming Tidyverse: readr package to import data (csv, tab-separated, fixed-width) (tidy-02)

Просмотров 3,8 тыс.5 лет назад

R Programming Tidyverse: readr package to import data (csv, tab-separated, fixed-width) (tidy-02)

Million dollar IRA: Relative strength (RSI) measures downside momentum; an avoidance signal (IRA-06)

Просмотров 9525 лет назад

Million dollar IRA: Relative strength (RSI) measures downside momentum; an avoidance signal (IRA-06)

how many types of synthetic securitization?

thanks!

Looks like the spreadsheet has been deleted

the file isn't there, it is showing deleted

I am talking about the excel workbook

hi, it says xls in dropbox was deleted... do you have another link? thanks alot. !!!!!!!!!!!!!! liked and subscribed !

The excel is not there at the location.

This is awesome! By the way, is the spreadsheet published online? Would love to play with it and develop some intuition

thank you !!!

Can you please share the sheet? The link says it was deleted. I’m unable to reproduce certain Inputs

A great video really solves many of my doubts

Hi im preparing for FRM, how to get study material for "bionic turtle " n FRM level 2 round??can u send me ur email? How do i get PDF download n ur tutorials on this??

The audio does not work for me

So you borrow money using a zero coupon bond multiplied by the strike. But how do you buy the shares when exercise / expiry if the share are worth more than the strike value that you borrowed? That part isn’t clear to me.

thanks

Thankyou for this insight as i here in Australia fell victim to a bank namely the ANZ via one of its agent iniciators Australian Wheat Board (AWB oil for food). ANZ as the ultimate beneficiary both bought and sold CDS on this lending structure then in 2009 created a massive swath of defaults by means of loan book restructure in actual fact potentially defaultig and liquidating 45% of the engaged tranches being 4,500 clients. Being mainly farmers the base asset (farmland) was added onto the super tranches at minimal cost as in liquidation (fire sale). I would like to forensically pick this apart as it not only invoved myself but wider corruption being AWB/ANZ and the Oil For Food scandal.

Thank you. That was crystal clear

Can I use GARCH (1,1) for portfolio returns, or GARCH (1,1) just applicable for a single security returns?

4:28 Why is the CDS „expensive“ when it's trading at only 2% and the other way around in a Positive basis trad?

hi David, thank you very much. Is it possible for you to re-upload the excel file? I think it has been deleted from Dropbox since. I would love to know, how you created the portfolio possibilities curve. Thank you!

Thank you

isn't it too much work and money for one little call premium?

the train is very cute! it made clearer.

AWESOMEEE

Great explainer, thank you!

How does the number is discounted to 4.367? Whats the step of the calculation?

Thank You!!

In a chooser option, where T1 would be the buy CALL or buy PUT, does the final value of the option remain the same? $ 10.890?

Excellent video, thanks a lot.. I have one doubt.. Is it possible to neutralize Gamma of a portfolio, using only SPY? In other words, how to calculate total Gamma of a portfolio, like we do with Delta-Beta (weighted Delta or Delta Dollars). Or in case of Gamma is only possible to neutralize individualy per underline position? What about Vega?

What's a calculator? 😅

Wouldn’t it be better for the writer of the options to only start hedging IF the price of the stock bridges the strike price? Because (assuming European style options) as long as the options ends up OTM then the options will expire worthless and all that unnecessary hedging won’t eat away the premium.

why in H27 you didn't do, to actualize, 5.000/((1+libor)^0.5)?

Very Great video. Thanks!

Thank you sooooo much for your help and all the excellently well organized lectures. You’re literally my best F&O TEACHER on RUclips!!!!! Thank you 🙏

Thanks for the wonderful explanation. Could you please Re-share the Excel link as on Dropbox it's deleted.

one of the best explanations!! thank you so much !!!

Super useful before exam!! 🎉 🎉

Nice explanation, as always. How about duration?

save mt life turtle man <3

16 year old video has the most coherent explaination of basis. Thanks!

In what situation would one use a par rate vs spot rate in their analysis or valuation of bonds/fixed-income securities?

This model seems to have a problem with the yield curves of 2024. Interpolation visually seems to be linear. Totally missing the inversion between 20 year and 30 year, and all years between 11 and 20. Good in the early years though.

What's the difference btw the 2 super senior tranches?

Why dont use boostraping for calculating forward rates?

if I have a negative NPV is this better for my US currency or worse : because the only way to get a negative NPV would be if we are paying a higher amount and receiving a lower amount giving me a negative premium. However other sources state that a negative premium/NPV value is in fact better for us as this means your premium as a cost will decrease by that much and therefore save you money. All in all my question is what does a negative NPV value mean good or bad for the US ? thank you

Gr8 Summary .. difficult concept but now getting it

Which version of John Hull's book do you use for this example?

Are all the returns log returns?

thank you so much

IIMB!!!!

the excel u use are immaculate ong